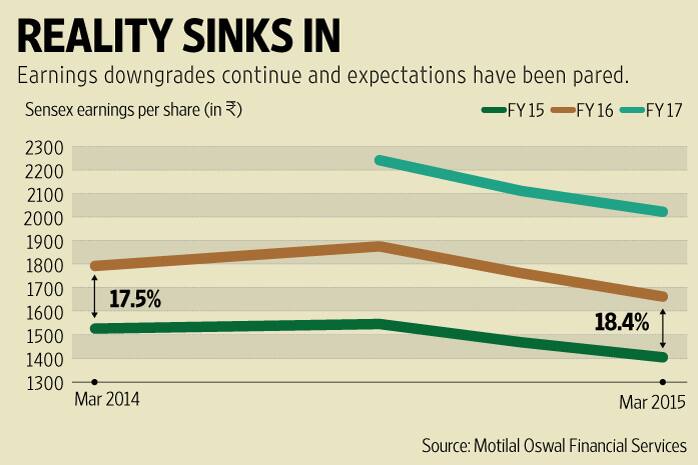

Earnings downgrades continue, for this year and next

Wednesday's drop in the Sensex ahead of the March quarter earnings is yet another warning that hope has surpassed reality in the Indian markets

Premium

Premium

Wednesday’s drop in the S&P BSE Sensex ahead of the March quarter earnings is yet another warning that hope has surpassed reality in the Indian markets. Earnings downgrades continue and expectations have been pared.

Indeed, earnings expectations had peaked towards the middle of the last fiscal year. A new government with a prime minister who was seen as decisive taking charge and a host of favourable factors such as declining inflation, a stable currency and lower oil and commodity prices acted as tailwinds for the markets. The Sensex climbed 19% in the first six months of the fiscal year 2015, only for reality to sink in.

Since then, there have been continuous downgrades as analysts noted that the economic recovery was getting delayed further. Despite some initial signs, on the ground investment demand recovery is yet to happen while rural consumption has been particularly hard hit because of several factors, the latest being unseasonal rains. Sales are expected to shrink in the March quarter for the first time in 5 years. No wonder then Sensex returns are just 8% in the six months since September.

The revisions to downgrades have happened to earnings of the current and next fiscal year as well. One consequence has been that, because of a sharper downward revision in FY15 earnings, earnings growth projected for the current fiscal year has gone up, owing to the base effect.

Unlock a world of Benefits! From insightful newsletters to real-time stock tracking, breaking news and a personalized newsfeed – it's all here, just a click away! Login Now!