Is pro-business reform necessarily pro-growth?

In an economy like India, with a severe overhang of socialism and central planning, basic pro-business reforms will almost surely enhance growth

Premium

Premium

Why is growth in the US and other advanced economies so anaemic even though the worst of the global financial crisis is now supposedly behind us?

Recently in Economics Express, I have explored in depth two popular explanations for this phenomenon. One explanation, known as secular stagnation, hypothesizes that it is deficient aggregate demand which explains the protracted stagnation in output and employment.

What would be required to cure it are sharply negative interest rates, which are difficult or impossible for the world’s central banks to deliver. This theory is most associated with Harvard economist and former White House adviser Lawrence Summers. (For more details, see here.)

The second popular explanation points to the slowing down in the growth of productivity—roughly, the amount of output that a given quantum of inputs can produce—as the key driver for stagnating output and employment in the US and other advanced economies.

According to this theory, slow or stagnant growth should be seen as the new normal. This theory is most associated with Northwestern University economist Robert Gordon. (For more details, see here.) As it happens, a recent news report that US productivity has actually fallen for the first time in 30 years lends some support to Gordon’s thesis.

These two explanations may be described as being Occidental, in that they may apply to the US and other advanced economies, but do not make much sense when applied to emerging economies such as India. Thus, even though the global technological frontier may be moving out more slowly than before, emerging economies are still far away from that frontier, and thus have a lot of room to grow rapidly as they catch up with international best practice.

Likewise, the idea that the problem is the inability of central banks to drive interest rates negative is implausible when applied to the emerging economies, which thus far have not needed to approach the zero lower bound, nor experiment with unconventional monetary policies such as quantitative easing.

Indeed, in India in particular, the embrace of flexible inflation targeting has been hailed as a major policy breakthrough in recent years, and this is about as conventional and neoclassical as monetary policy could be. (For a recent analysis of inflation targeting in India, see here.)

As it happens, there is a third explanation afoot that tries to explain stagnating growth in the US, and this particular one has much more resonance and relevance when applied to emerging economies such as India. It is has also aroused a great deal of controversy.

In a recent op-ed in The Wall Street Journal, economist John Cochrane has argued that the real culprit to explain anaemic growth is not deficient demand or slowing productivity, neither of which is easily amenable to viable policy options, but rather, excessive and burdensome regulation, which clearly is within the ambit of public policy.

As Cochrane writes: “If it takes years to get the permits to start projects and mountains of paper to hire people, if every step risks a new criminal investigation, people don’t invest, hire or innovate." His proposed remedy is a “dramatic legal and regulatory simplification, restoring the rule of law", what he describes as “simple common-sense, Adam Smith policies".

Now both the prescription and remedy likely make sense in an over-regulated country such as India (more on which below), in which socialism and central planning still cast a long shadow, but how well do they fit the US? That country, arguably, is the closest to being a free market bastion among the world’s major economies. Is Cochrane’s argument thus more ideology than analysis? This is at the heart of an ongoing debate that his article has sparked off.

It is worth recalling that Cochrane, formerly a professor at the University of Chicago’s Booth School of Business and currently a fellow at the Hoover Institution at Stanford, is an influential economist on the right in the US, and, predictably, his prognosis and policy advice have raised the hackles of economists on the left.

Most prominent among these is Berkeley economist Bradford DeLong, who in a recent blog post has gone to the extent of blasting both Cochrane and The Wall Street Journal as “unprofessional".

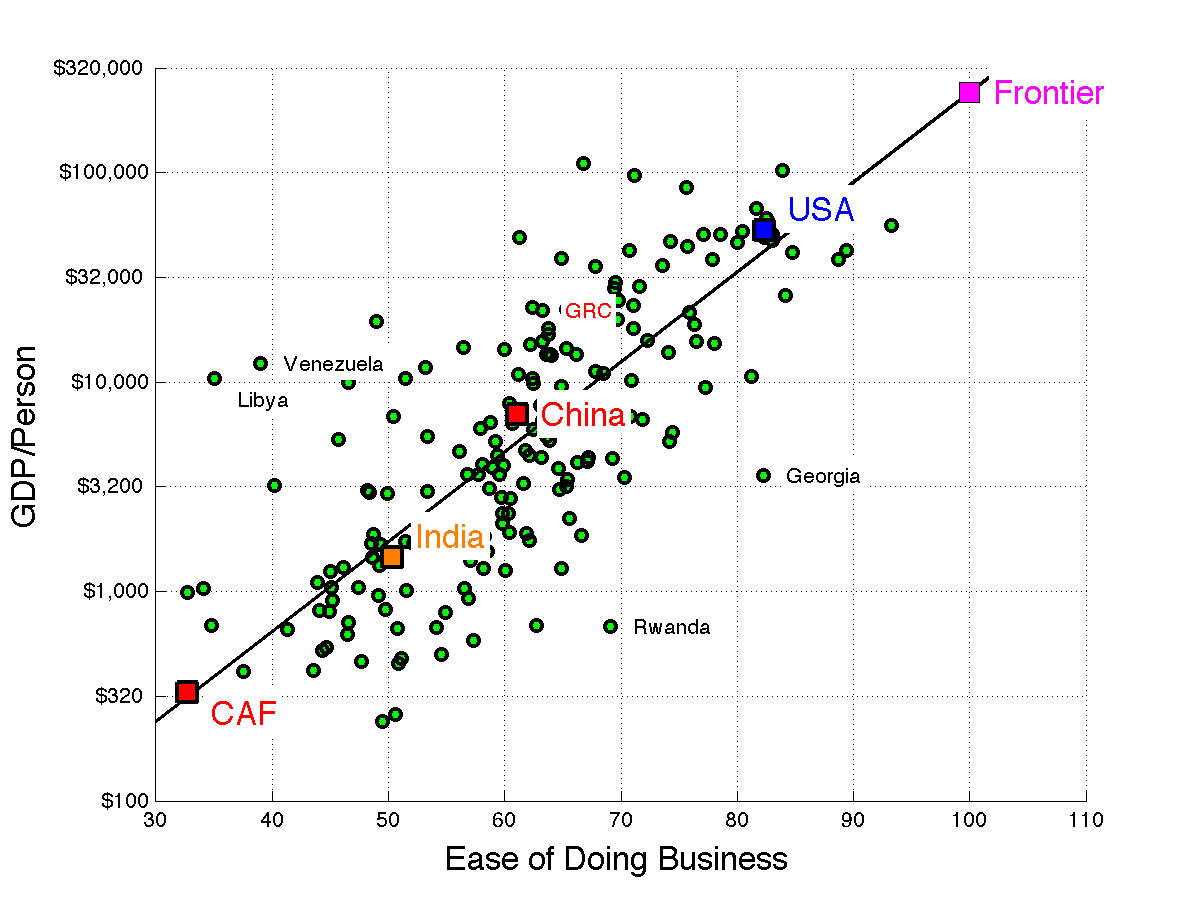

The heart of the dispute concerns Cochrane’s claim that, if the US were to move to the frontier score of 100 in the World Bank’s Ease of Doing Business (EDB) “distance to frontier" index, this would correspond to a per capita income of $163,000. This is 209% higher than current US per capita income, and could be realized by 6% additional annual growth in per capita income over the next 20 years.

Further, if the US could somehow best the frontier, and move up to 110, the implied level of per capita income would be a whopping $400,000, 650% better than now, or 15% extra growth per year for the next 20 years.

(For the wonkish: the World Bank EDB study reports its findings in two main ways: the much publicized ranking from 1 to 189, and a scientifically more useful “distance to frontier" index with 0 being the worst and 100 being the frontier. It is this latter measure which Cochrane uses in his analysis.)

Cochrane reaches these conclusions by plotting a regression between the natural logarithm of income per capita in the year 2014 in the 189 countries covered by the World Bank’s EDB report and the corresponding “distance to frontier" score for each of those countries in the same year.

His graph showing the regression line and the scatter of points being fitted may be found here, with Cochrane building on his op-ed in a blog post. It is this graph, essentially, which forms the basis for Cochrane to make claims about how much income per capita in the US would jump if it moved to or beyond the frontier.

Now, the dispute between Cochrane and DeLong hangs on a technical point. In Cochrane’s analysis, as I note, he plots the natural logarithm of income per capita on the vertical axis against the EDB “distance to frontier" score on the horizontal axis.

In contrast, DeLong’s graph, found here, plots the level, not the logarithm, of income per capita against the “distance to frontier" score (technically, using a cubic polynomial fit, not a linear fit). This is what allows DeLong to argue that Cochrane’s claim of the potential income gain from moving out to the frontier is outlandishly high.

Think of it as the battle of the duelling graphs or the battle of logarithms versus levels!

As it happens, there is no single “right" or “wrong" methodology in mapping a regression of one variable against another: it depends on the judgement of the researcher as to which is more plausible or appropriate for the problem at hand. Cochrane’s log-linear regression makes his claim look very plausible, whereas DeLong’s regression in levels make it looks highly implausible.

The other dimension of DeLong’s critique of Cochrane is that a correlation between the ease of doing business and per capita income does not necessarily imply a causal relationship running from the former to the latter; the causality could run in the opposite direction, or both variables could be jointly determined by other underlying factors missing from the regression.

Meanwhile, Cochrane has responded to DeLong in this blog post, in which he argues both that his logarithmic specification accords with how economists normally model growth and that it is plausible to believe that there is at least some causal relationship between the ease of doing business and income per capita, albeit not a perfect one.

Understandably, the Cochrane-DeLong feud has generated a slew of reactions from economists, commentators and bloggers on both sides of the fence. One thoughtful take is in this blog post by Princeton undergraduate student Evan Soltas, who argues, plausibly, that improvements which boost a country’s ease of doing business score should not be seen as a substitute for deeper structural reforms which go beyond reforms narrowly designed to improve the doing business climate.

(Of course, Cochrane and his defenders could argue that, in a heavily regulated economy, starting with improving the doing business climate will for the most part work in the same direction as deeper structural reforms and so is a reasonable proxy in the first instance, an argument to which I return later.)

Interestingly, the Cochrane-DeLong dispute in the case of the US, which boils down to a debate over whether pro-business reforms are also pro-market and pro-growth, has a long and venerable history in India, and, indeed, is still current to this day.

Thus, the canonical story of India’s growth miracle points to the structural economic reforms initiated after the 1991 macroeconomic crisis, which swept away the worst excesses of the licence-permit-quota raj. This story is well told by economists Jagdish Bhagwati and Arvind Panagariya in their recent book, Why Growth Matters.

Bhagwati, my own guru, is a professor of economics at Columbia University, widely seen as the intellectual godfather of the 1991 liberalization and frequently mentioned as a Nobel contender, while Panagariya, on leave from Columbia, is an eminent trade economist and at present vice-chairperson of the NITI Aayog.

However, a contrary view propounded by economists Dani Rodrik of the Harvard Kennedy School and Arvind Subramanian, then of the International Monetary Fund (IMF), as articulated in various places including in this 2004 research paper, holds that the real impetus for growth came almost a decade earlier, from a pro-business attitude shift during the latter Indira Gandhi and then the Rajiv Gandhi eras, rather than the structural pro-market reforms undertaken during the P.V. Narasimha Rao and Atal Bihari Vajpayee eras.

A version of this thesis is echoed in remarks made in 2004 by Raghuram Rajan, then economic counsellor of the IMF, also pointing to the 1980s, rather than 1991, as an important turning point. (Interestingly, in a more recent 2012 piece, he emphasized the structural reforms of 1991 and onward as key to India’s growth spurt.)

Similar arguments were also made by Princeton political scientist Atul Kohli in a pair of articles in the Economic and Political Weekly (“Politics of Economic Growth in India, 1980-2005", Parts I and II, 1 and 8 April 2006, archived here and here).

While my own view on this debate is not a secret—in various places, including in this 2010 article, I have argued on the side of Bhagwati-Panagariya—it would be fair to say that the two sets of explanations may be understood as complementary rather than competing. In other words, the structural reforms of 1991 and thereafter were perhaps abetted by a pro-business attitude shift originating in the 1980s.

Also, while it is true that the statistical evidence marshalled by Rodrik and Subramanian suggests a structural break in the data occurred in the 1980s, signalling this as the decade in which growth began to pick up, one could argue that the growth pick-up which began in the 1980s required the structural reforms of 1991 and on to sustain itself. Indeed, Bhagwati and Panagariya have made such an argument in their book.

What is more, the key linkage from the older Bhagwati-Panagariya versus Rodrik-Subramanian debate in India to the current Cochrane versus DeLong debate in the US is to note that the latter are not principally debating attitudes towards business, but the extent to which regulation burdensome to business is a major drag on economic growth.

Of course, one could argue that an attitude antithetical to business is one driver of regulation that places undue burdens on business, but this armchair sociological explanation would miss the deeper political economy account of rent-seeking and crony capture in the US which Cochrane in particular, in a grand Chicago tradition, highlights.

Again, the crux of the Cochrane-DeLong dispute, with which we began, is the extent to which a series of business-friendly reforms—which would presumably lead to a jump towards the frontier in the World Bank’s EDB “distance to frontier" measure—will be a major impetus to economic growth.

And, as it happens, this unresolved empirical question bears directly on the Narendra Modi government’s oft-repeated aspiration to boost India in the World Bank EDB rankings, which was reiterated again recently, as reported here.

Taking a leaf from DeLong’s methodological objections to Cochrane’s analysis, does the Modi government’s aspiration make sense?

This is where economic wisdom must meet basic common sense. In an economy with an overhang of socialism and central planning as severe as India’s, basic reforms which make it easier to do business—such as eliminating wasteful and burdensome red tape and reducing if not eliminating corruption, along with improving basic infrastructure—are almost surely going to be growth-enhancing.

If, as evidence suggests, a pro-business tilt in the 1980s gave a boost to growth and paved the way in some sense for the 1991 reforms, then one could well harbour the hope that the pro-business reforms initiated by the Modi government augur well for the future.

One thing is for certain: the debate about whether pro-business reforms are indeed pro-market and ultimately pro-growth, which lie at the heart of the Cochrane-DeLong dispute, are central to as yet unresolved policy debates in India, as we have seen. And, what is more, they speak directly to the likely efficacy in terms of a future growth kick of the pro-business stance of the Modi government as exemplified in its commitment to improve the doing business climate.

Economics Express runs weekly, and features interesting reads from the world of economics and finance.

Comments are welcome at feedback@livemint.com

Unlock a world of Benefits! From insightful newsletters to real-time stock tracking, breaking news and a personalized newsfeed – it's all here, just a click away! Login Now!

{kind=link}