Industry

Industry

Why small public sector banks are on the divestment radar

Summary

- The five smallest of the 12 state-owned banks are less strategically important to the government and have been improving their financial performance.

In her 2021 Budget speech, finance minister Nirmala Sitharaman said the government would privatize two public sector banks. News reports have suggested that these could be from among the following five: Central Bank of India, Indian Overseas Bank, Bank of Maharashtra, UCO Bank, and Punjab and Sind Bank. Divestment of these relatively small banks may not draw strong protests and their good growth and profitability metrics make them attractive to buyers. But gaps remain. The government is setting up a panel to identify the banks for divestment, The Economic Times reported recently.

Government Holding

At current share prices, the central government can raise ₹28,000-54,000 crore by reducing its stake to 26% in two of these five banks. The actual amount will depend on the banks chosen and sale price.

This is still a fraction of what it can raise from stake sales in larger PSU banks. At current prices, it can raise ₹31,395 crore by selling 6% in State Bank of India (SBI), the largest PSU bank by assets.

But the government can only think of selling another 6% in SBI. Its current shareholding in SBI is 57.6%, and it would not like to go below 51%, for economic and political reasons. The same is the case with Punjab National Bank (73% stake) and Bank of Baroda (63%), the next-biggest PSU banks by assets. In the five small PSU banks, the government owns more than 90%, and a majority stake sale would be politically more palatable, though not easy.

Asset Growth

Total assets of small private banks grew by 9.1% in 2022-23, driven by a jump in loans and advances, which were up by 24%.

Even the two top banks among the smaller lot, Central Bank of India and Indian Overseas Bank, saw their loans and advances grow by over 20%, even as their total assets grew in mid-single digits. Bank of Maharashtra reported the highest growth in total assets among all PSU banks.

Reflecting the rest of the banking sector, loans and advances grew despite higher interest rates, thanks to greater economic activity. This growth is an indicator of the improving financial health of these banks and would help in their eventual sale. At the same time, they are still too small to be of strategic importance to the government.

The total assets of SBI are larger than the assets of these five banks put together.

Widening Margins

Importantly, the smaller PSU banks are also making more money, a measure of which is the ‘net interest margin’. NIM measures the difference between the interest income generated by banks and the interest paid out to their lenders (principally, depositors), relative to the amount of their interest-earning assets. On average, in 2022-23, the NIM of large PSU banks went up by 29 basis points. The NIM of smaller PSU banks increased by 25 basis points, with UCO Bank (0.03%) and Punjab and Sind Bank (-0.01%) being a drag.The same is reflected in profits, too. The cumulative net profit of all PSU banks crossed ₹1 trillion for the first time in 2022-23, up 57% from the previous fiscal. Again, SBI accounted for about half the profits, underscoring the strategic importance of big banks in general and SBI in particular.

Shrinking NPAs

The improvement in profitability didn’t just come from growth. In 2022-23, smaller PSU banks not only reduced net NPAs (non-performing assets) to a greater extent than their larger peers, they also reported lower net NPAs. For these five small banks, net NPAs fell by 1.2 percentage points (pp) over 2021-22 and 2.6 pp over 2020-21 (compared to 1.17 pp and 2.17 pp, respectively, for large PSU banks).

On average, the five small PSU banks had net NPAs of 1.39% in 2022-23, compared to 1.47% for large PSU banks.Lowering NPAs in PSU banks has been a core element of the government’s so-called 4R strategy of recognition, resolution, recapitalization and reforms.

Net NPAs refer to the loans held by banks that are not generating expected returns due to non-payment or default by borrowers. It is an indicator of the quality of a bank’s loan portfolio and also impacts its ability to lend.

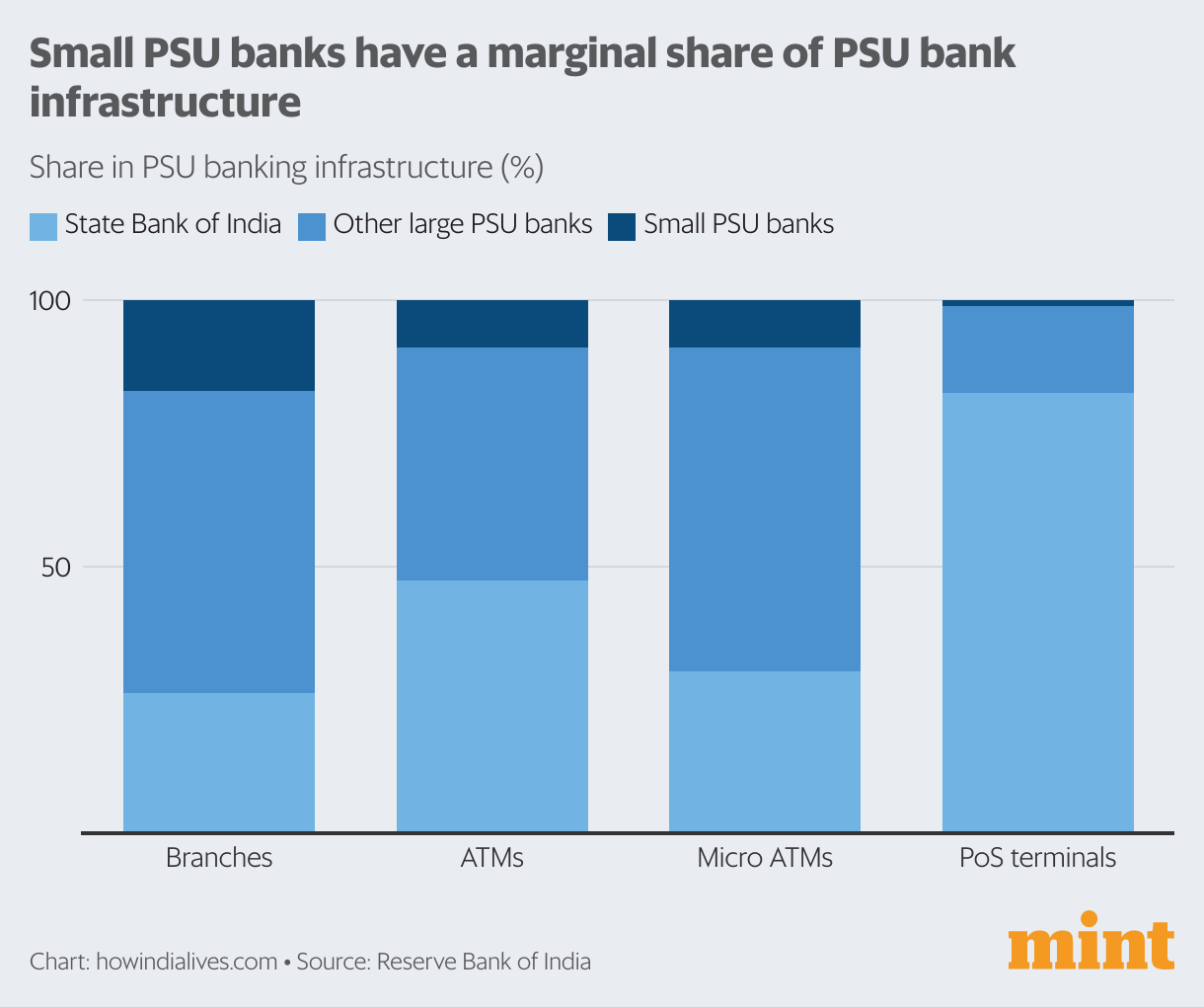

Infra Woes

This set of five small PSU banks accounts for 17% of all PSU bank branches. Beyond them, SBI accounts for 26.4% and other PSU banks the rest. Interestingly, SBI accounts for a disproportionately large number of ATMs, point-of-sale (PoS) terminals and micro ATMs. The five small PSU banks have a lesser share of this infrastructure in relation to their number of branches. ATMs, PoS terminals and micro ATMs are cheaper than setting up branches, and are increasingly becoming more capable of offering other banking services. Lower investments by small PSU banks in other infrastructure is partly a result of their financial constraints. However, as the sector gets more competitive, smaller banks will have to strengthen their own infrastructure or partner with other entities to compete. Or, they will be absorbed into larger banks, as the government wants.

www.howindialives.com is a database and search engine for public data.